While the broader market has struggled with the S&P 500 down 1.7% since October 2024, Duolingo has surged ahead as its stock price has climbed by 14.5% to $326.71 per share. This performance may have investors wondering how to approach the situation.

Following the strength, is DUOL a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Is DUOL a Good Business?

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

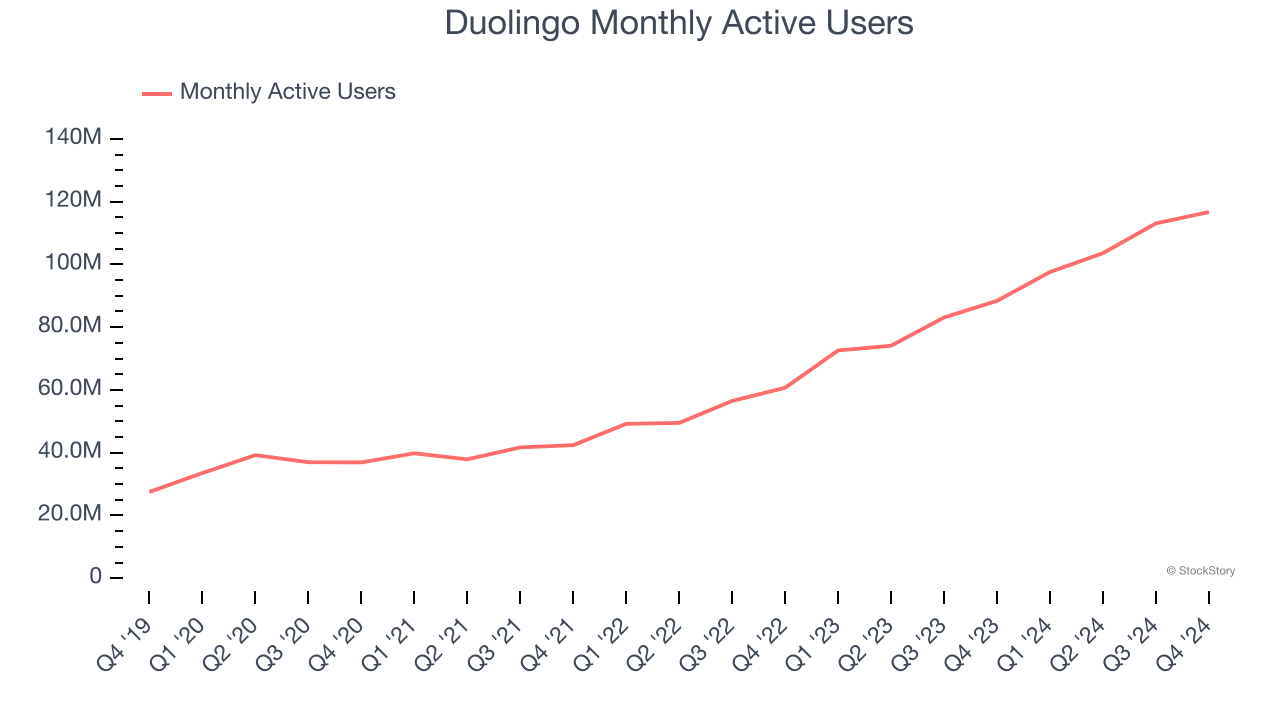

1. Monthly Active Users Skyrocket, Fueling Growth Opportunities

As a subscription-based app, Duolingo generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Duolingo’s monthly active users, a key performance metric for the company, increased by 41.5% annually to 116.7 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

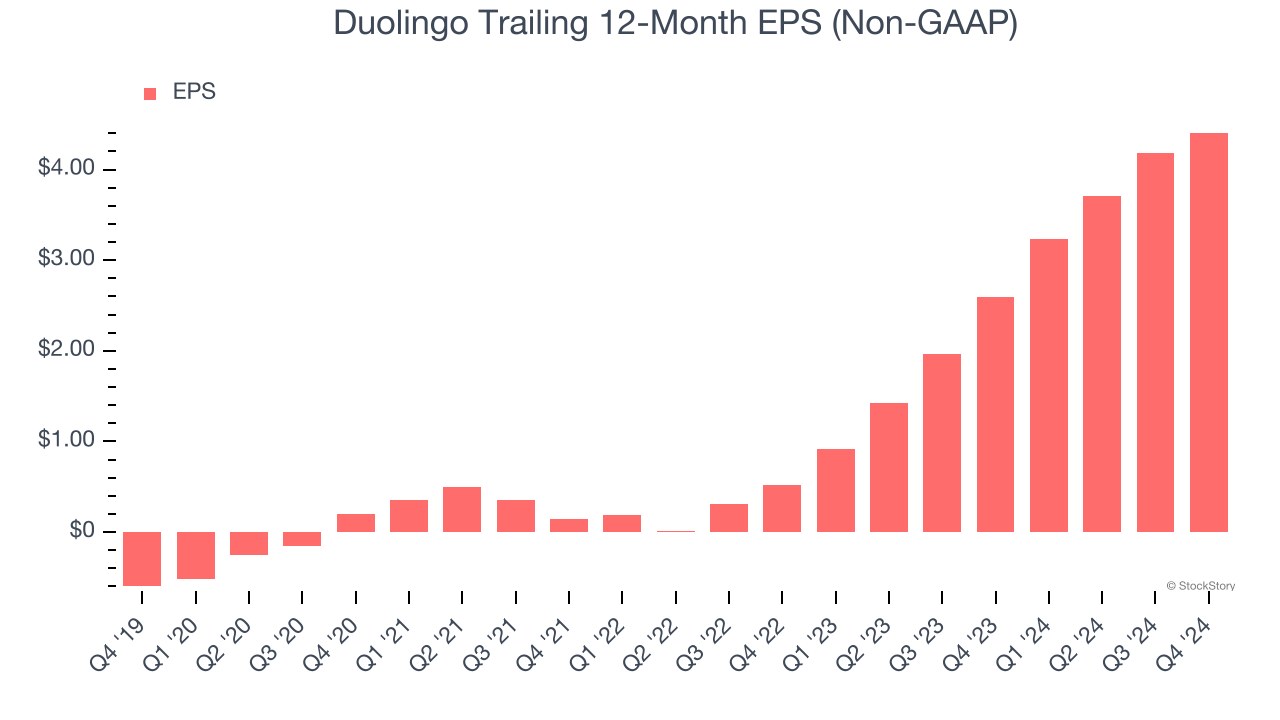

2. Outstanding Long-Term EPS Growth

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Duolingo’s EPS grew at an astounding 210% compounded annual growth rate over the last three years, higher than its 44% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

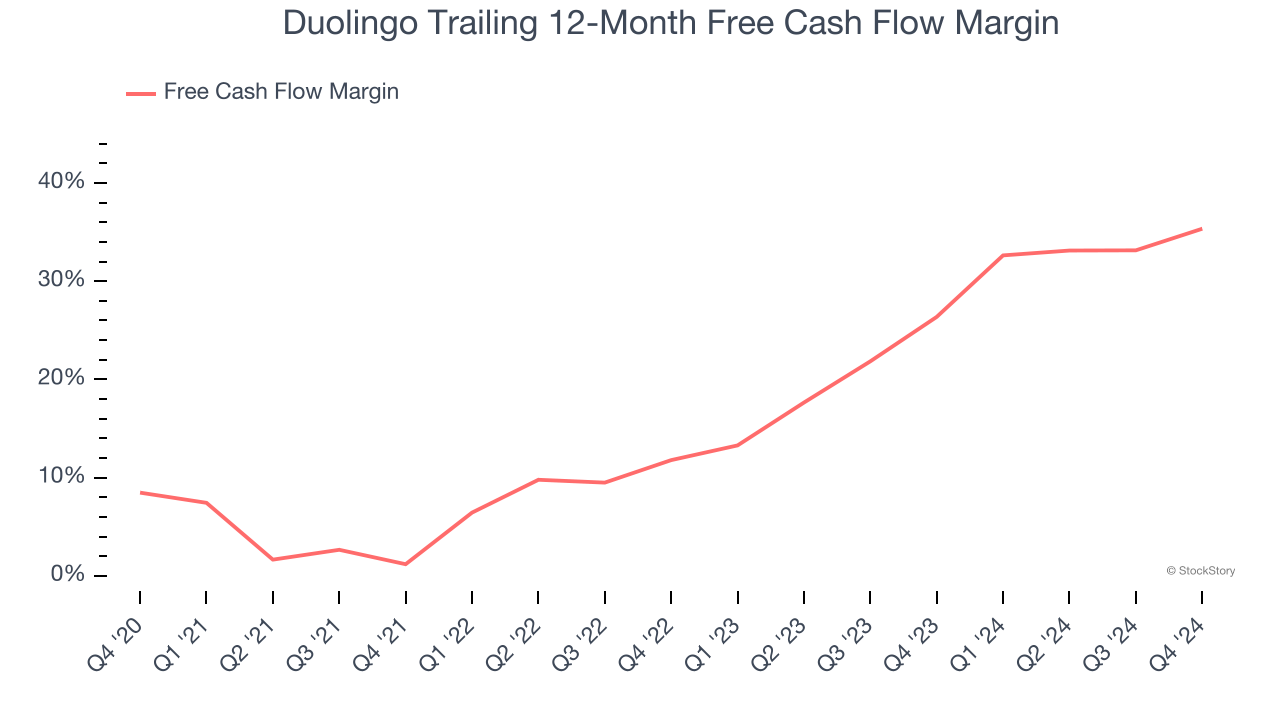

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Duolingo has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 31.6% over the last two years.

Final Judgment

These are just a few reasons why we think Duolingo is one of the best consumer internet companies out there, and with its shares beating the market recently, the stock trades at 54.2× forward EV-to-EBITDA (or $326.71 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Duolingo

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.