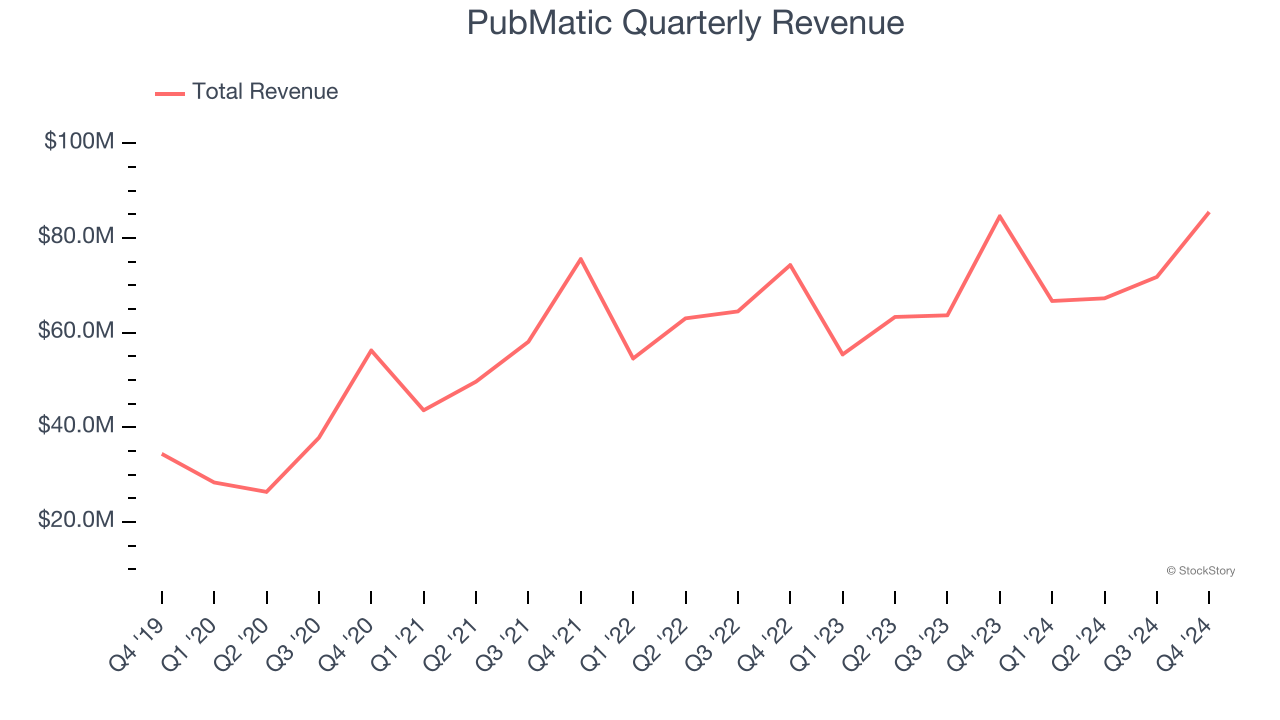

Programmatic advertising platform Pubmatic (NASDAQ: PUBM) missed Wall Street’s revenue expectations in Q4 CY2024 as sales only rose 1.1% year on year to $85.5 million. Next quarter’s revenue guidance of $62 million underwhelmed, coming in 5.9% below analysts’ estimates. Its non-GAAP profit of $0.41 per share was 9.6% above analysts’ consensus estimates.

Is now the time to buy PubMatic? Find out by accessing our full research report, it’s free.

PubMatic (PUBM) Q4 CY2024 Highlights:

- Revenue: $85.5 million vs analyst estimates of $88.27 million (1.1% year-on-year growth, 3.1% miss)

- Adjusted EPS: $0.41 vs analyst estimates of $0.37 (9.6% beat)

- Adjusted EBITDA: $37.65 million vs analyst estimates of $35.61 million (44% margin, 5.7% beat)

- Revenue Guidance for Q1 CY2025 is $62 million at the midpoint, below analyst estimates of $65.87 million

- EBITDA guidance for Q1 CY2025 is $6 million at the midpoint, below analyst estimates of $8.81 million

- Operating Margin: 17.3%, down from 24.1% in the same quarter last year

- Free Cash Flow Margin: 10.4%, up from 4% in the previous quarter

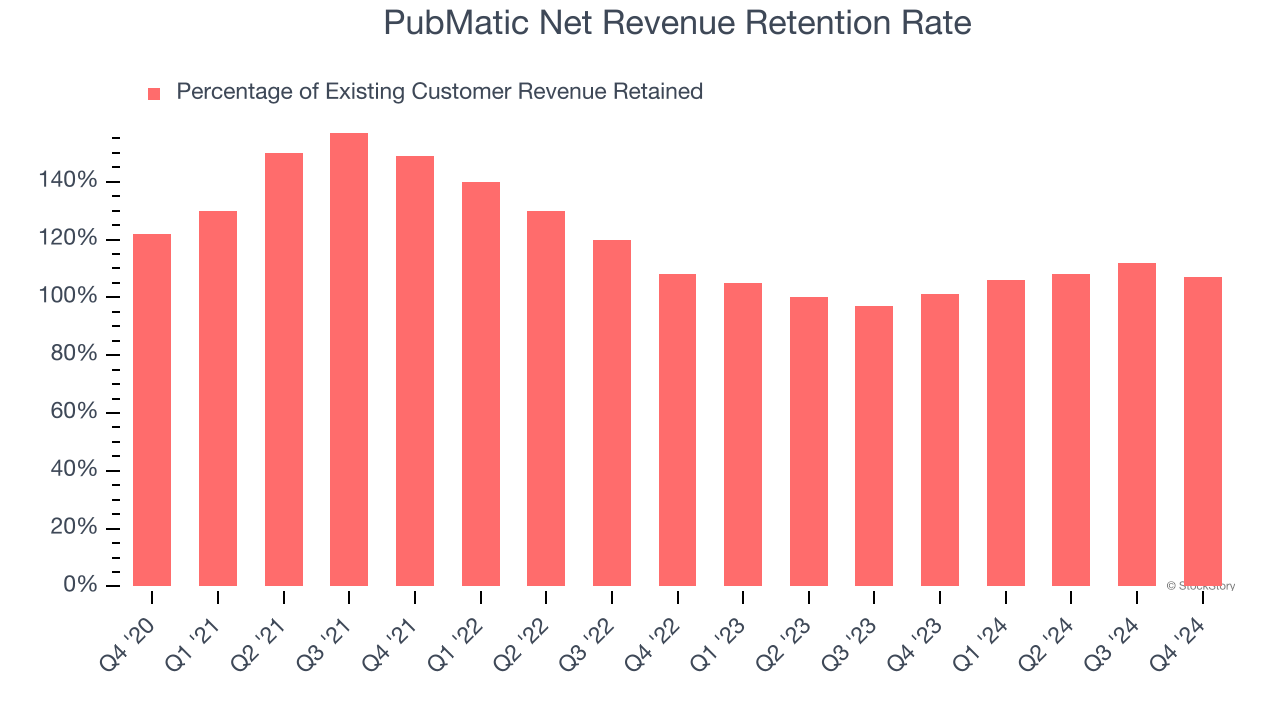

- Net Revenue Retention Rate: 107%, down from 112% in the previous quarter

- Market Capitalization: $687.4 million

“Revenue growth in the year more than doubled over 2023, driven by strength in CTV, emerging revenue streams, and marquee customers choosing PubMatic to build and scale their ad businesses. Our revenue mix is evolving; in the fourth quarter, CTV more than doubled to 20% of total revenue. These achievements mark an inflection point in our underlying business that highlights critical scale on our platform and a significant shift in ad buying toward channels with the highest consumer engagement such as CTV, mobile app and commerce media,” said Rajeev Goel, co-founder and CEO at PubMatic.

Company Overview

Founded in 2006 as an online ad platform helping ad sellers, Pubmatic (NASDAQ: PUBM) is a fully integrated cloud-based programmatic advertising platform.

Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, PubMatic’s 8.7% annualized revenue growth over the last three years was sluggish. This was below our standard for the software sector and is a tough starting point for our analysis.

This quarter, PubMatic’s revenue grew by 1.1% year on year to $85.5 million, falling short of Wall Street’s estimates. Company management is currently guiding for a 7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, similar to its three-year rate. This projection is underwhelming and indicates its newer products and services will not catalyze better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

PubMatic’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 108% in Q4. This means PubMatic would’ve grown its revenue by 8.3% even if it didn’t win any new customers over the last 12 months.

Trending up over the last year, PubMatic has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from PubMatic’s Q4 Results

We enjoyed seeing PubMatic beat analysts’ EPS and EBITDA expectations this quarter. On the other hand, its revenue and EBITDA guidance for next quarter fell short of Wall Street’s estimates. We note that ad tech companies had weaker quarters in general, as both The Trade Desk and DoubleVerify missed on revenue and guided below for next quarter. PubMatic wasn't spared, and the stock traded down 9.1% to $12.70 immediately following the results.

PubMatic underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.