As the Q3 earnings season wraps, let’s dig into this quarter’s best and worst performers in the construction and maintenance services industry, including Concrete Pumping (NASDAQ:BBCP) and its peers.

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years–. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

The 13 construction and maintenance services stocks we track reported a slower Q3. As a group, revenues missed analysts’ consensus estimates by 1%.

Luckily, construction and maintenance services stocks have performed well with share prices up 12.5% on average since the latest earnings results.

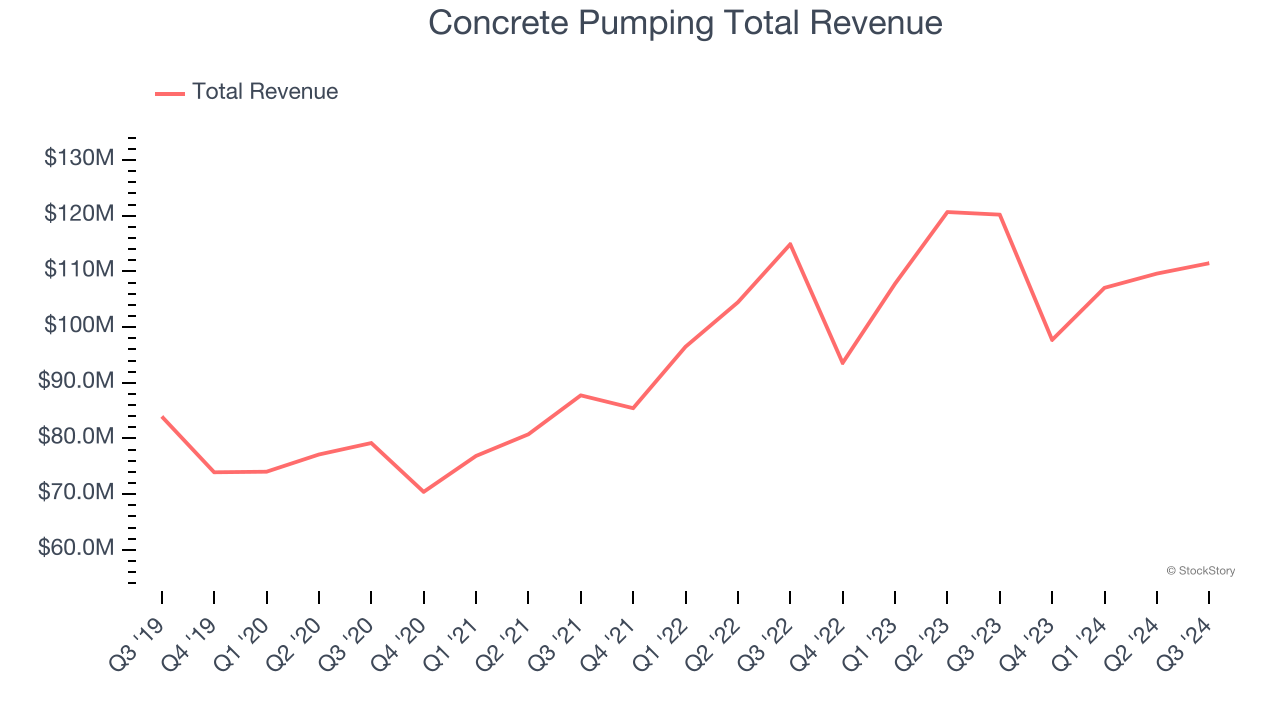

Concrete Pumping (NASDAQ:BBCP)

Going public via SPAC in 2018, Concrete Pumping (NASDAQ:BBCP) is a provider of concrete pumping and waste management services in the United States and the United Kingdom.

Concrete Pumping reported revenues of $111.5 million, down 7.3% year on year. This print exceeded analysts’ expectations by 1.1%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ adjusted operating income estimates but a significant miss of analysts’ organic revenue estimates.

"In the fourth quarter, continued double-digit organic growth in our U.S. Concrete Waste Management business was offset by volume-driven declines in our U.S. Concrete Pumping segment," said Bruce Young, CEO of CPH.

The stock is up 31.1% since reporting and currently trades at $8.48.

Is now the time to buy Concrete Pumping? Access our full analysis of the earnings results here, it’s free.

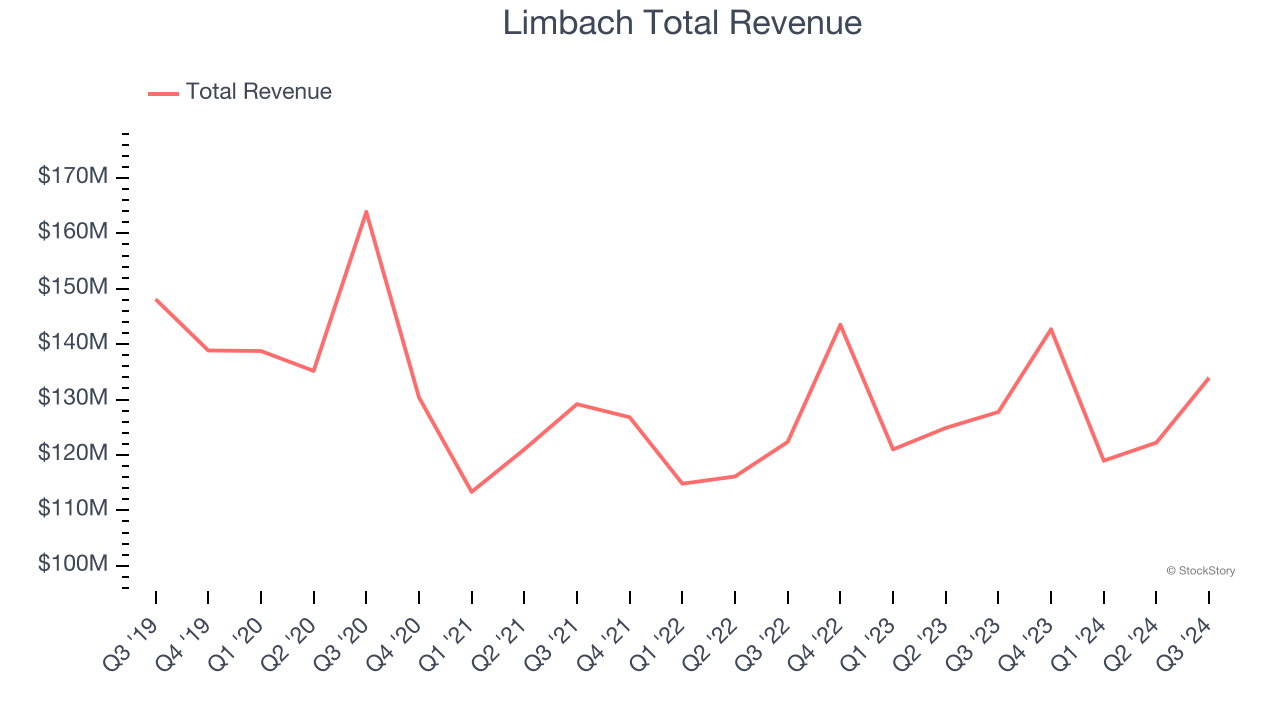

Best Q3: Limbach (NASDAQ:LMB)

Established in 1901, Limbach (NASDAQ: LMB) provides integrated building systems solutions, including mechanical, electrical, and plumbing services.

Limbach reported revenues of $133.9 million, up 4.8% year on year, outperforming analysts’ expectations by 3.4%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Limbach delivered the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 22.2% since reporting. It currently trades at $95.33.

Is now the time to buy Limbach? Access our full analysis of the earnings results here, it’s free.

Tutor Perini (NYSE:TPC)

Known for constructing the Philadelphia Eagles’ Stadium, Tutor Perini (NYSE:TPC) is a civil and building construction company offering diversified general contracting and design-build services.

Tutor Perini reported revenues of $1.08 billion, up 2.1% year on year, falling short of analysts’ expectations by 7.2%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

Tutor Perini delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 13.8% since the results and currently trades at $26.10.

Read our full analysis of Tutor Perini’s results here.

Construction Partners (NASDAQ:ROAD)

Founded in 2001, Construction Partners (NASDAQ:ROAD) is a civil infrastructure company that builds and maintains roads, highways, and other infrastructure projects.

Construction Partners reported revenues of $538.2 million, up 13.3% year on year. This print came in 0.6% below analysts' expectations. Zooming out, it was a mixed quarter as it also logged full-year EBITDA guidance beating analysts’ expectations but a miss of analysts’ EPS estimates.

The stock is down 12.5% since reporting and currently trades at $79.95.

Read our full, actionable report on Construction Partners here, it’s free.

APi (NYSE:APG)

Started in 1926 as an insulation contractor, APi (NYSE:APG) provides life safety solutions and specialty services for buildings and infrastructure.

APi reported revenues of $1.83 billion, up 2.4% year on year. This number missed analysts’ expectations by 3.4%. Overall, it was a softer quarter as it also produced a significant miss of analysts’ organic revenue estimates and full-year revenue guidance missing analysts’ expectations.

The stock is up 15% since reporting and currently trades at $38.18.

Read our full, actionable report on APi here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.