As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the home construction materials industry, including Quanex (NYSE:NX) and its peers.

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

The 12 home construction materials stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 0.7%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.3% since the latest earnings results.

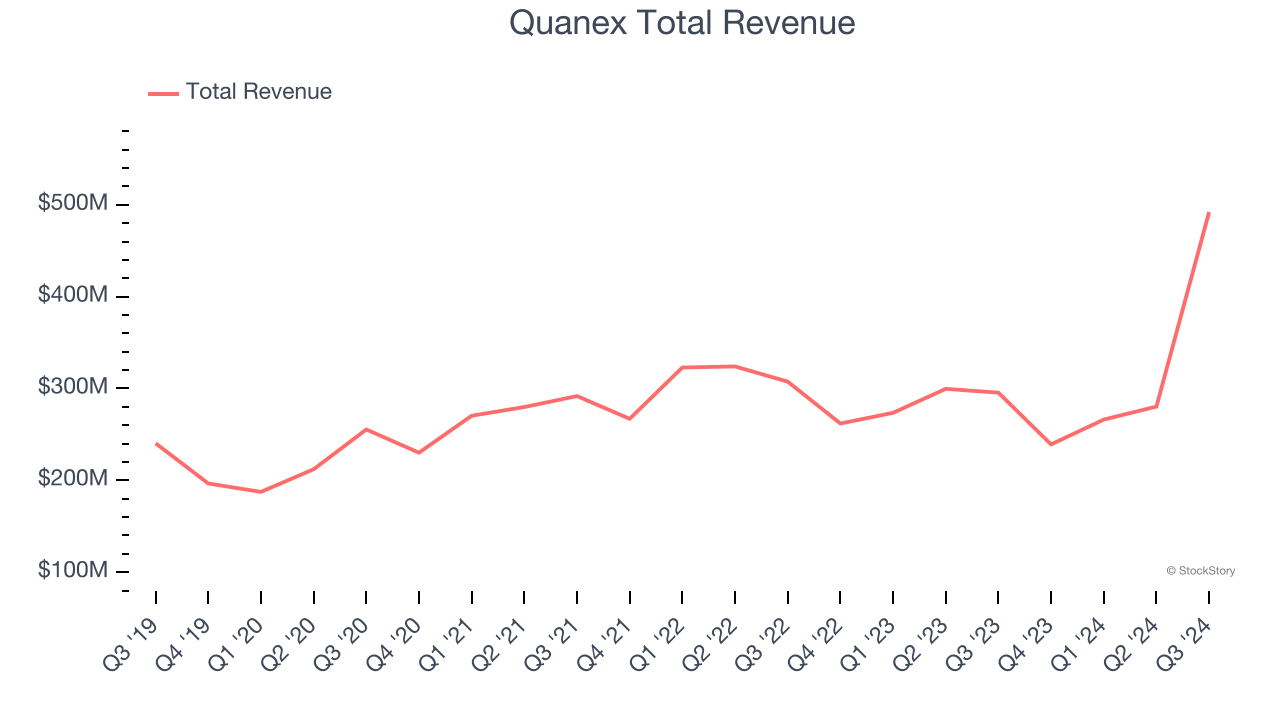

Quanex (NYSE:NX)

Starting in the seamless tube industry, Quanex (NYSE:NX) manufactures building products like window, door, kitchen, and bath cabinet components.

Quanex reported revenues of $492.2 million, up 66.6% year on year. This print was in line with analysts’ expectations, and overall, it was a very strong quarter for the company with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

Quanex scored the fastest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 24.9% since reporting and currently trades at $21.72.

Is now the time to buy Quanex? Access our full analysis of the earnings results here, it’s free.

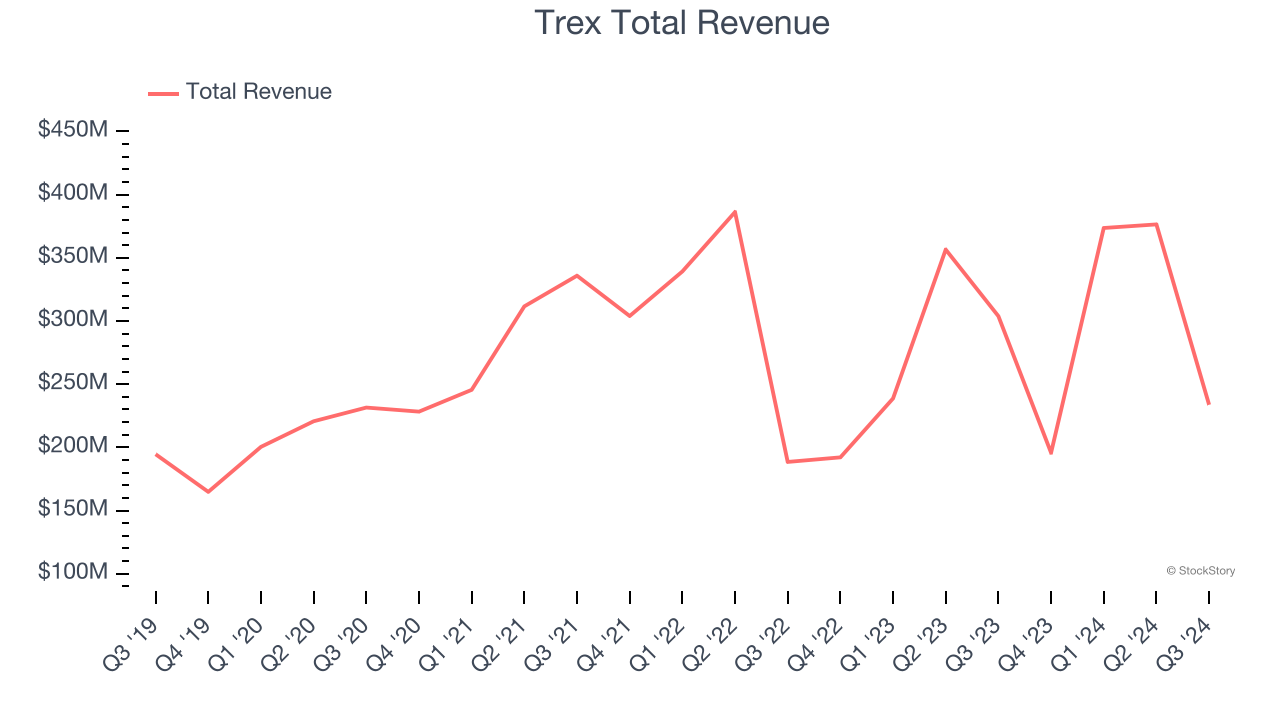

Best Q3: Trex (NYSE:TREX)

Addressing the demand for aesthetically-pleasing and unique outdoor living spaces, Trex Company (NYSE:TREX) makes wood-alternative decking, railing, and patio furniture.

Trex reported revenues of $233.7 million, down 23.1% year on year, outperforming analysts’ expectations by 3.3%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA estimates.

Trex pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 11.4% since reporting. It currently trades at $74.06.

Is now the time to buy Trex? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: JELD-WEN (NYSE:JELD)

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE:JELD) manufactures doors, windows, and other related building products.

JELD-WEN reported revenues of $934.7 million, down 13.2% year on year, falling short of analysts’ expectations by 6.2%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

JELD-WEN delivered the weakest full-year guidance update in the group. As expected, the stock is down 33.7% since the results and currently trades at $9.37.

Read our full analysis of JELD-WEN’s results here.

Hayward (NYSE:HAYW)

Credited with introducing the first variable-speed pool pump, Hayward (NYSE:HAYW) makes residential and commercial pool equipment and accessories.

Hayward reported revenues of $227.6 million, up 3.3% year on year. This print beat analysts’ expectations by 2.1%. It was a very strong quarter as it also logged a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ EPS estimates.

Hayward scored the highest full-year guidance raise among its peers. The stock is up 3.3% since reporting and currently trades at $15.26.

Read our full, actionable report on Hayward here, it’s free.

Griffon (NYSE:GFF)

Initially in the defense industry, Griffon (NYSE:GFF) is a now diversified company specializing in home improvement, professional equipment, and building products.

Griffon reported revenues of $659.7 million, up 2.9% year on year. This result surpassed analysts’ expectations by 2.9%. Overall, it was a very strong quarter as it also recorded an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

The stock is up 14% since reporting and currently trades at $77.70.

Read our full, actionable report on Griffon here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.