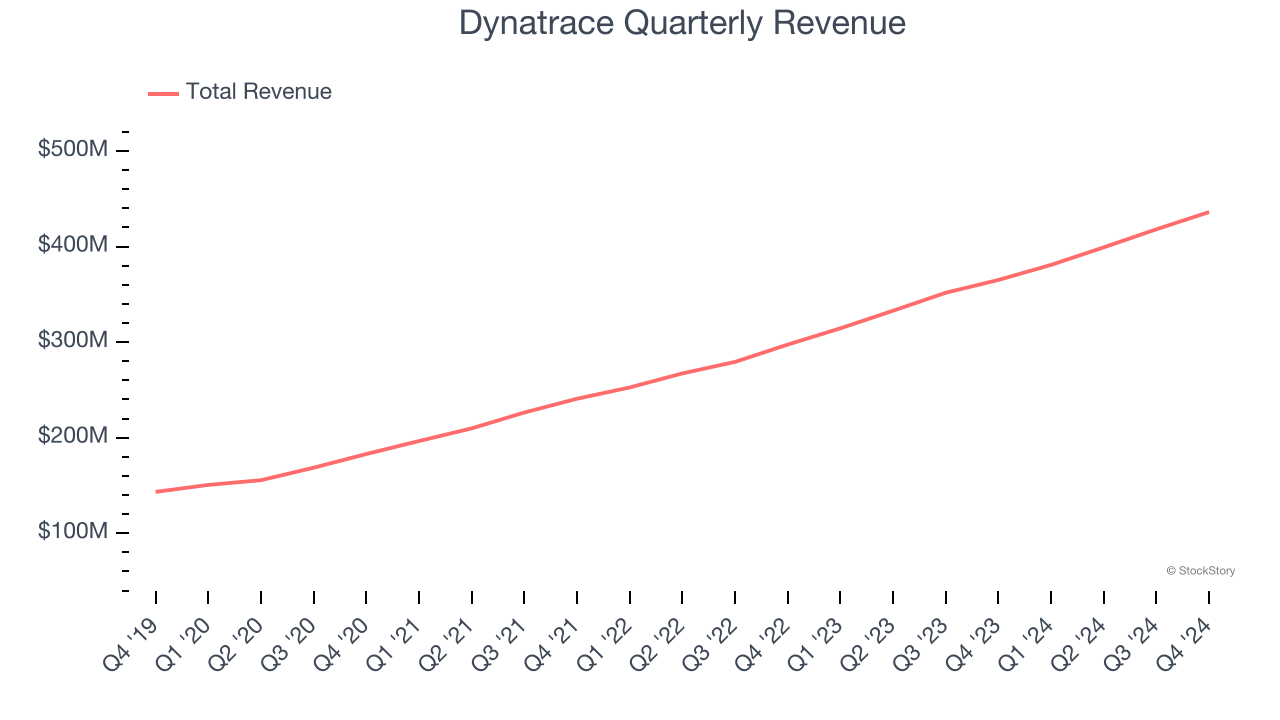

Application performance monitoring software provider Dynatrace (NYSE:DT) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 19.5% year on year to $436.2 million. Guidance for next quarter’s revenue was better than expected at $434.5 million at the midpoint, 1.7% above analysts’ estimates. Its non-GAAP profit of $0.37 per share was 11.7% above analysts’ consensus estimates.

Is now the time to buy Dynatrace? Find out by accessing our full research report, it’s free.

Dynatrace (DT) Q4 CY2024 Highlights:

- Revenue: $436.2 million vs analyst estimates of $426.4 million (19.5% year-on-year growth, 2.3% beat)

- Adjusted EPS: $0.37 vs analyst estimates of $0.33 (11.7% beat)

- Adjusted Operating Income: $130.7 million vs analyst estimates of $119.2 million (30% margin, 9.6% beat)

- Revenue Guidance for Q1 CY2025 is $434.5 million at the midpoint, above analyst estimates of $427.1 million

- Management raised its full-year Adjusted EPS guidance to $1.37 at the midpoint, a 3.4% increase

- Operating Margin: 10.9%, up from 9.8% in the same quarter last year

- Free Cash Flow Margin: 8.6%, up from 4.8% in the previous quarter

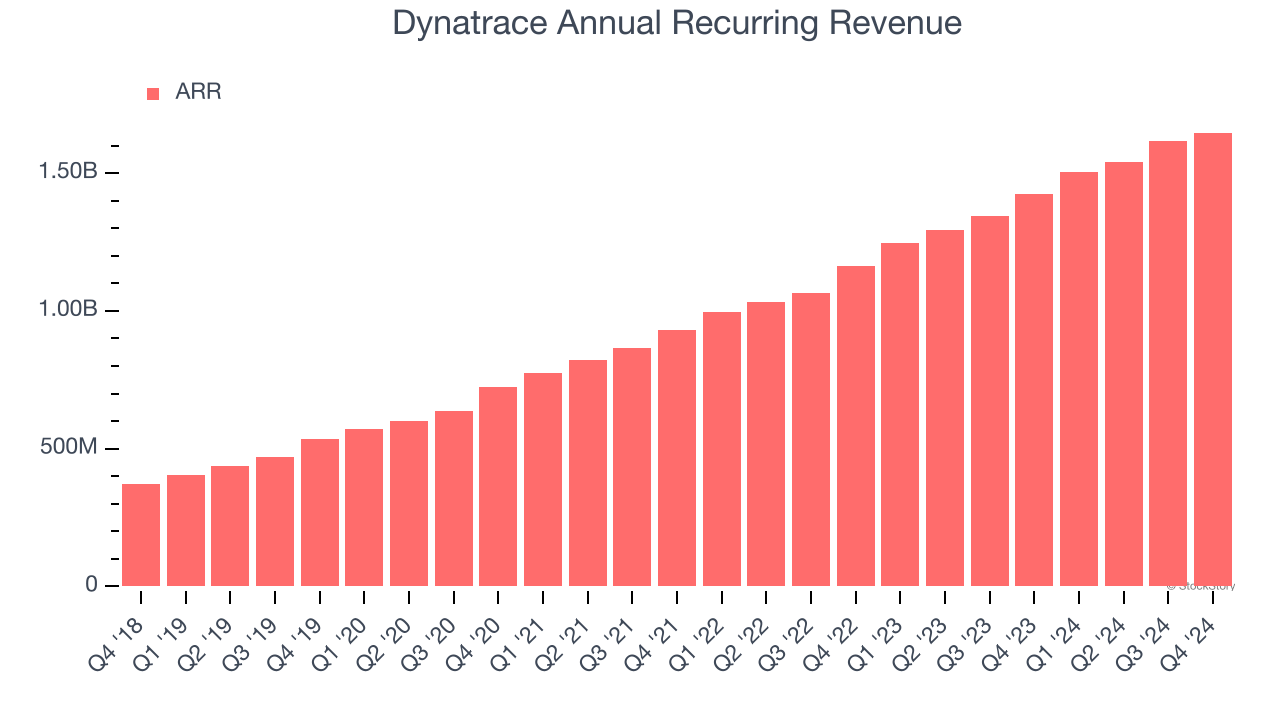

- Annual Recurring Revenue: $1.65 billion at quarter end, up 15.6% year on year

- Billings: $467.1 million at quarter end, up 4% year on year

- Market Capitalization: $17.12 billion

"Our third quarter results exceeded guidance across all key operating metrics," said Rick McConnell, Chief Executive Officer of Dynatrace.

Company Overview

Founded in Austria in 2005, Dynatrace (NYSE:DT) provides companies with software that allows them to monitor the performance of their full technology stack, from software applications to the infrastructure they run on.

Cloud Monitoring

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical and ever more complex. To solve this challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with the visibility to troubleshoot issues in real-time.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Dynatrace’s sales grew at a decent 23.2% compounded annual growth rate over the last three years. Its growth was slightly above the average software company and shows its offerings resonate with customers.

This quarter, Dynatrace reported year-on-year revenue growth of 19.5%, and its $436.2 million of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 14.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.2% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is commendable and implies the market is factoring in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Dynatrace’s ARR punched in at $1.65 billion in Q4, and over the last four quarters, its growth was impressive as it averaged 18.9% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Dynatrace a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Dynatrace is quite efficient at acquiring new customers, and its CAC payback period checked in at 29.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a strong brand reputation, giving it more resources pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Dynatrace’s Q4 Results

We were impressed by Dynatrace’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also glad its EPS guidance for next quarter came in higher than Wall Street’s estimates. On the other hand, its billings missed and its annual recurring revenue fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed. The market seemed to focus on the negative topline metrics, and the stock traded down 2.1% to $56.24 immediately after reporting.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.