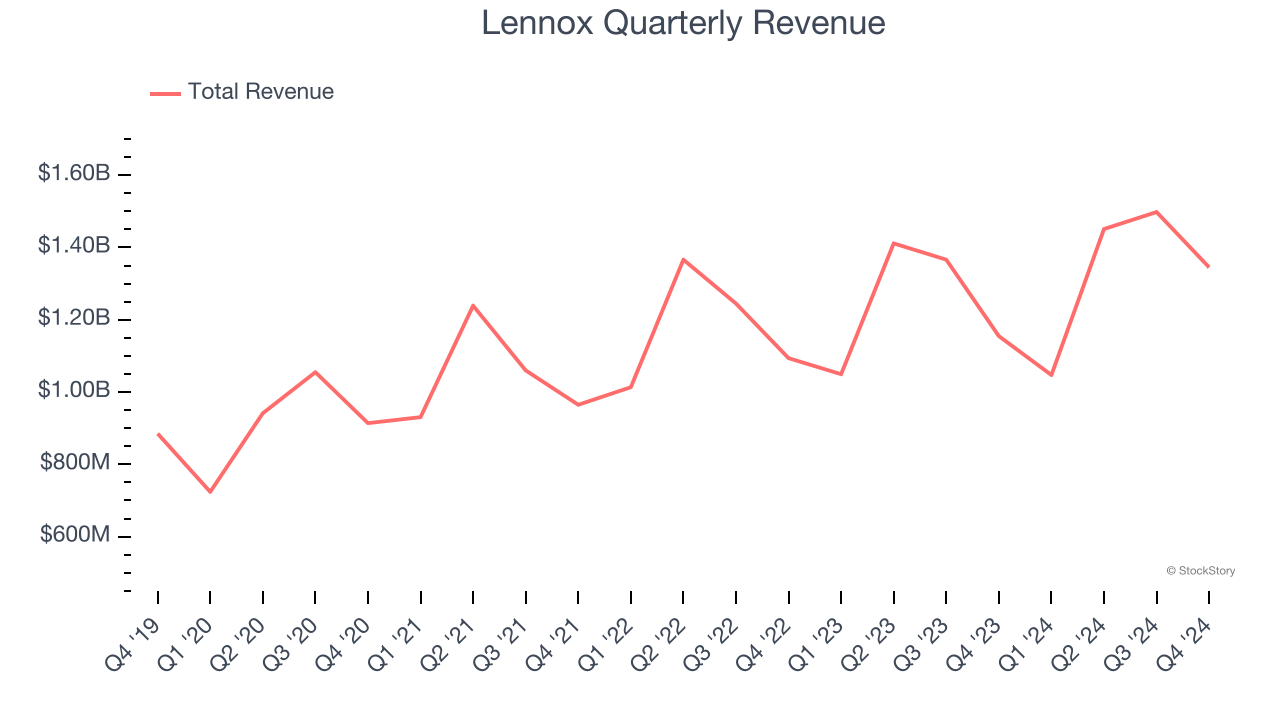

Climate control solutions innovator Lennox International (NYSE:LII) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 16.5% year on year to $1.35 billion. Its non-GAAP profit of $5.60 per share was 32% above analysts’ consensus estimates.

Is now the time to buy Lennox? Find out by accessing our full research report, it’s free.

Lennox (LII) Q4 CY2024 Highlights:

- Revenue: $1.35 billion vs analyst estimates of $1.24 billion (16.5% year-on-year growth, 8.9% beat)

- Adjusted EPS: $5.60 vs analyst estimates of $4.24 (32% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $22.75 at the midpoint, missing analyst estimates by 2%

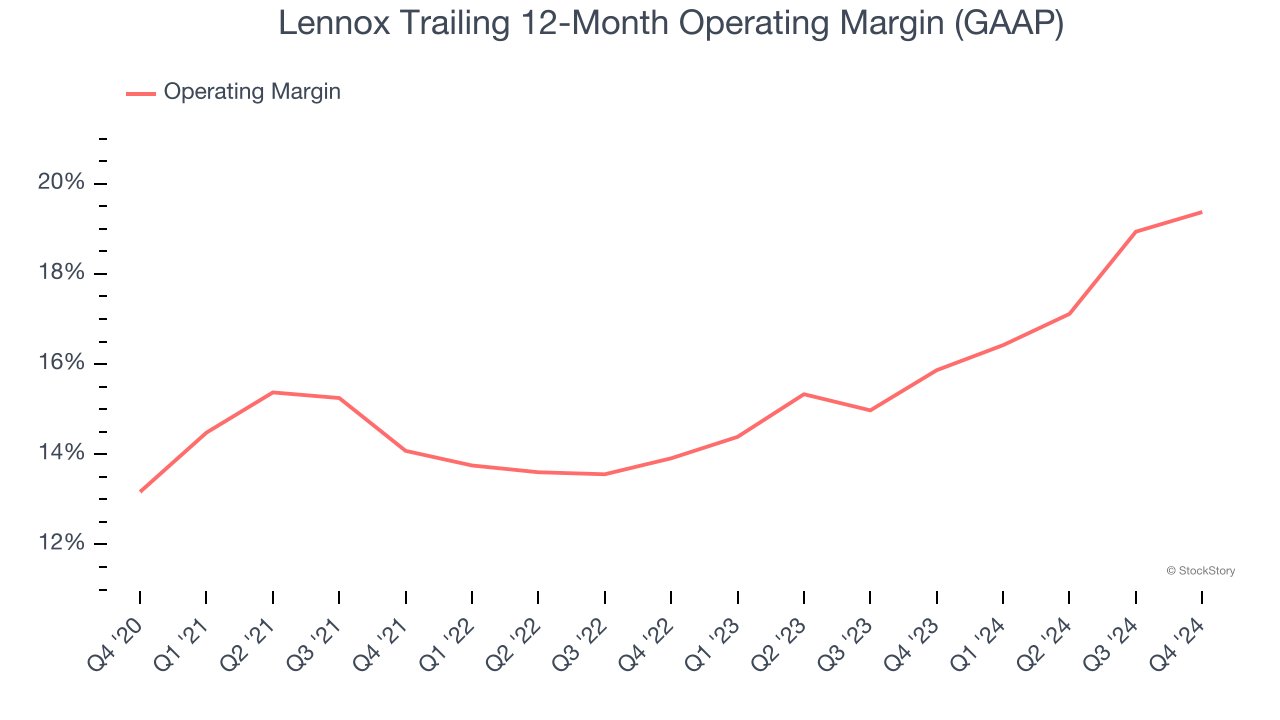

- Operating Margin: 18.2%, up from 16% in the same quarter last year

- Free Cash Flow Margin: 20.2%, up from 15.7% in the same quarter last year

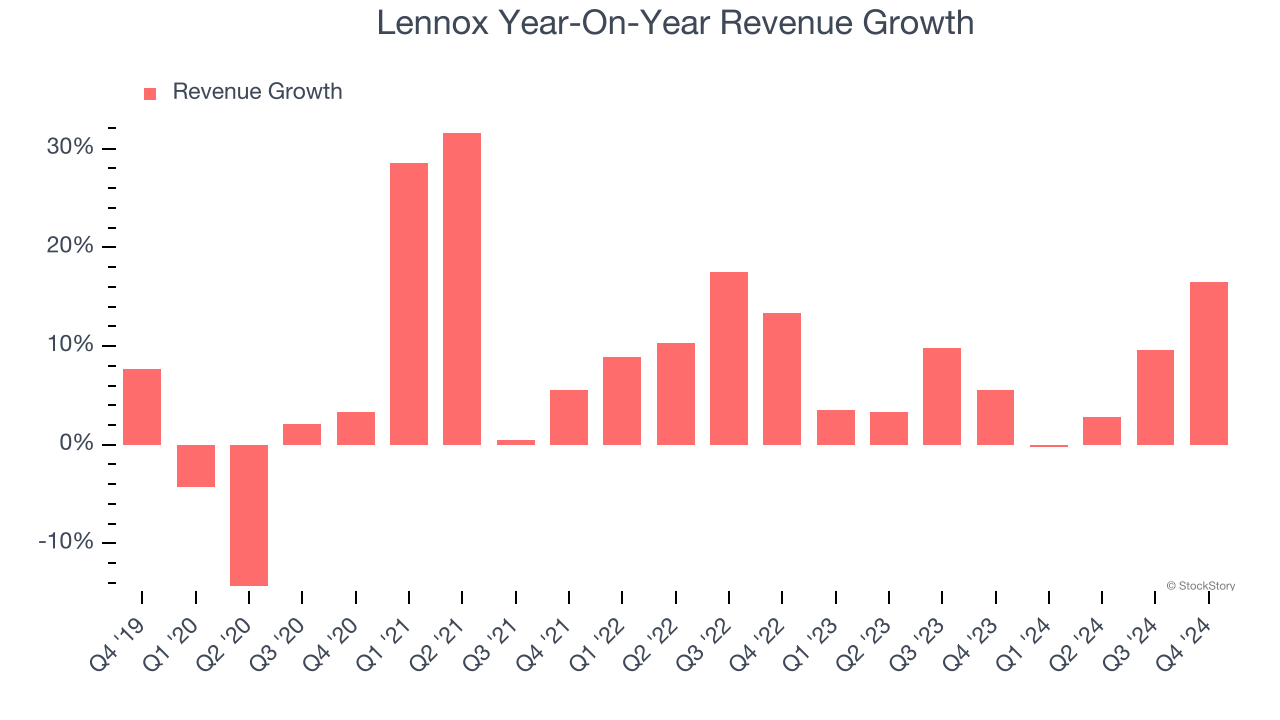

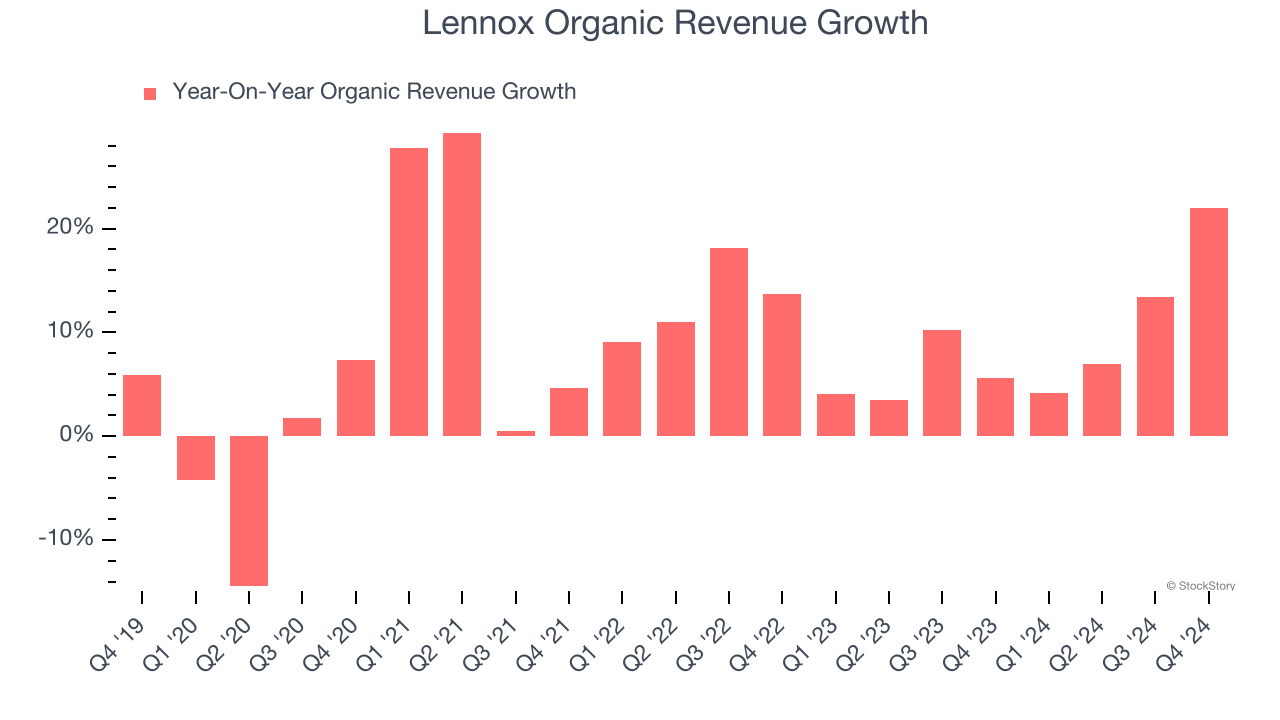

- Organic Revenue rose 22% year on year (5.6% in the same quarter last year)

- Market Capitalization: $23.6 billion

"2024 was a remarkable year filled with record achievements, and last quarter continued that momentum as we delivered impressive results across the board," said CEO, Alok Maskara.

Company Overview

Based in Texas and founded over a century ago, Lennox (NYSE:LII) is a climate control solutions company offering heating, ventilation, air conditioning, and refrigeration (HVACR) goods.

HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Lennox’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Lennox’s annualized revenue growth of 6.4% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, Lennox’s organic revenue averaged 8.7% year-on-year growth. Because this number is better than its normal revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Lennox reported year-on-year revenue growth of 16.5%, and its $1.35 billion of revenue exceeded Wall Street’s estimates by 8.9%.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Lennox has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.5%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Lennox’s operating margin rose by 6.2 percentage points over the last five years, showing its efficiency has meaningfully improved.

In Q4, Lennox generated an operating profit margin of 18.2%, up 2.1 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

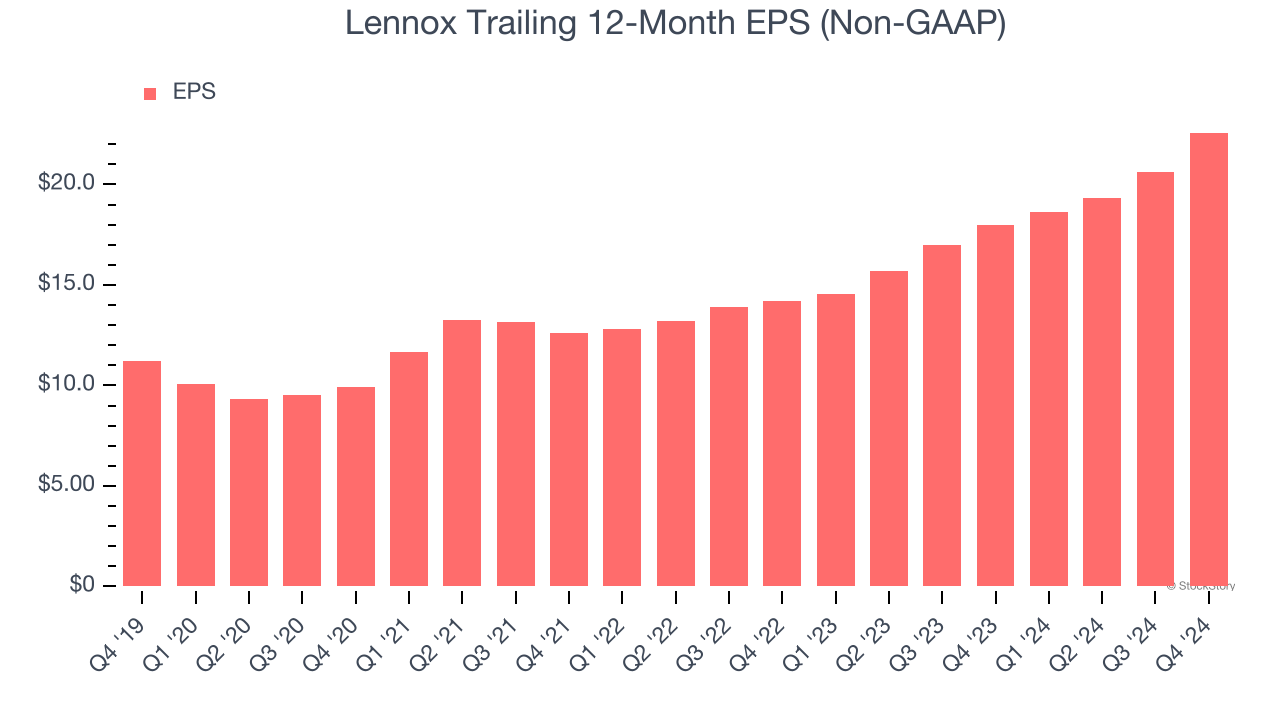

Lennox’s EPS grew at a spectacular 15.1% compounded annual growth rate over the last five years, higher than its 7.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

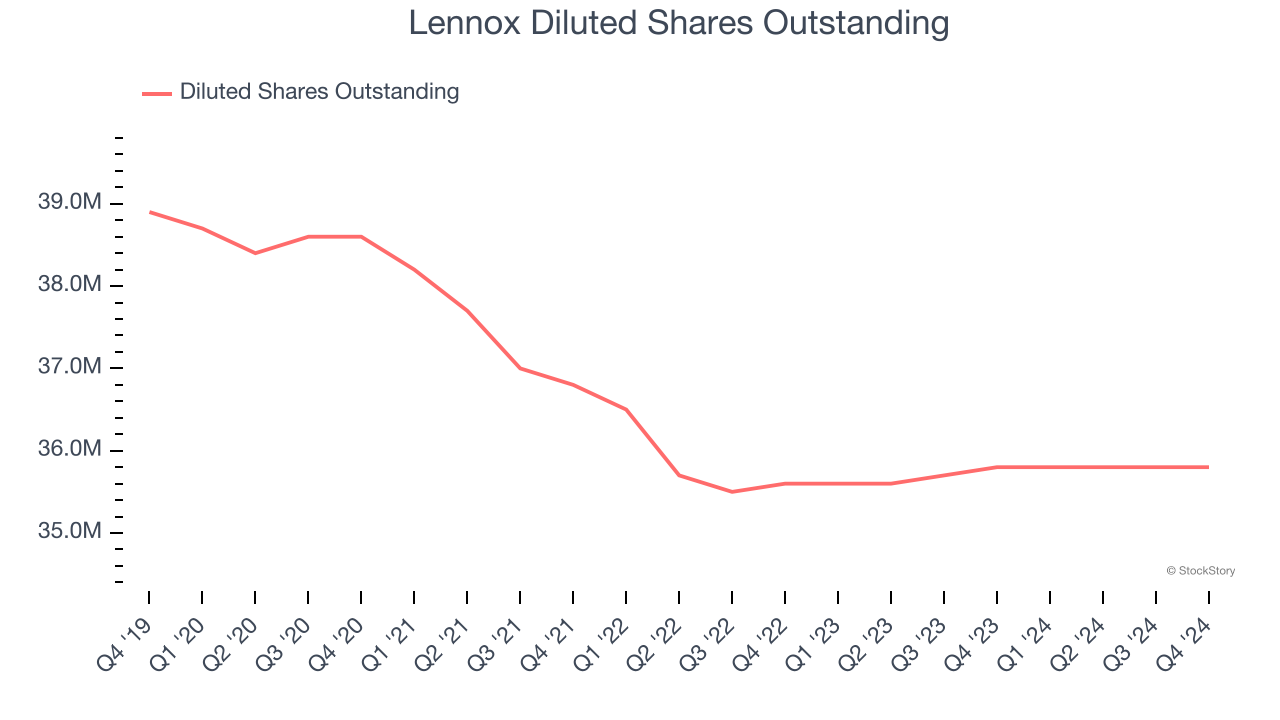

Diving into Lennox’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Lennox’s operating margin expanded by 6.2 percentage points over the last five years. On top of that, its share count shrank by 8%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Lennox, its two-year annual EPS growth of 26.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Lennox reported EPS at $5.60, up from $3.63 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Lennox’s full-year EPS of $22.58 to grow 3.2%.

Key Takeaways from Lennox’s Q4 Results

We were impressed by how significantly Lennox blew past analysts’ organic revenue expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance missed. Zooming out, we think this quarter featured some important positives. The stock traded up 2% to $675.75 immediately after reporting.

Lennox may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.