Casual restaurant chain Brinker International (NYSE:EAT) reported Q4 CY2024 results exceeding the market’s revenue expectations, with sales up 26.5% year on year to $1.36 billion. The company’s full-year revenue guidance of $5.2 billion at the midpoint came in 6.1% above analysts’ estimates. Its non-GAAP profit of $2.80 per share was 50.9% above analysts’ consensus estimates.

Is now the time to buy Brinker International? Find out by accessing our full research report, it’s free.

Brinker International (EAT) Q4 CY2024 Highlights:

- Revenue: $1.36 billion vs analyst estimates of $1.24 billion (26.5% year-on-year growth, 9.6% beat)

- Adjusted EPS: $2.80 vs analyst estimates of $1.86 (50.9% beat)

- Adjusted EBITDA: $215.8 million vs analyst estimates of $157.7 million (15.9% margin, 36.8% beat)

- The company lifted its revenue guidance for the full year to $5.2 billion at the midpoint from $4.73 billion, a 10.1% increase

- Management raised its full-year Adjusted EPS guidance to $7.75 at the midpoint, a 44.9% increase

- Operating Margin: 11.5%, up from 5.8% in the same quarter last year

- Free Cash Flow Margin: 12.4%, up from 4.5% in the same quarter last year

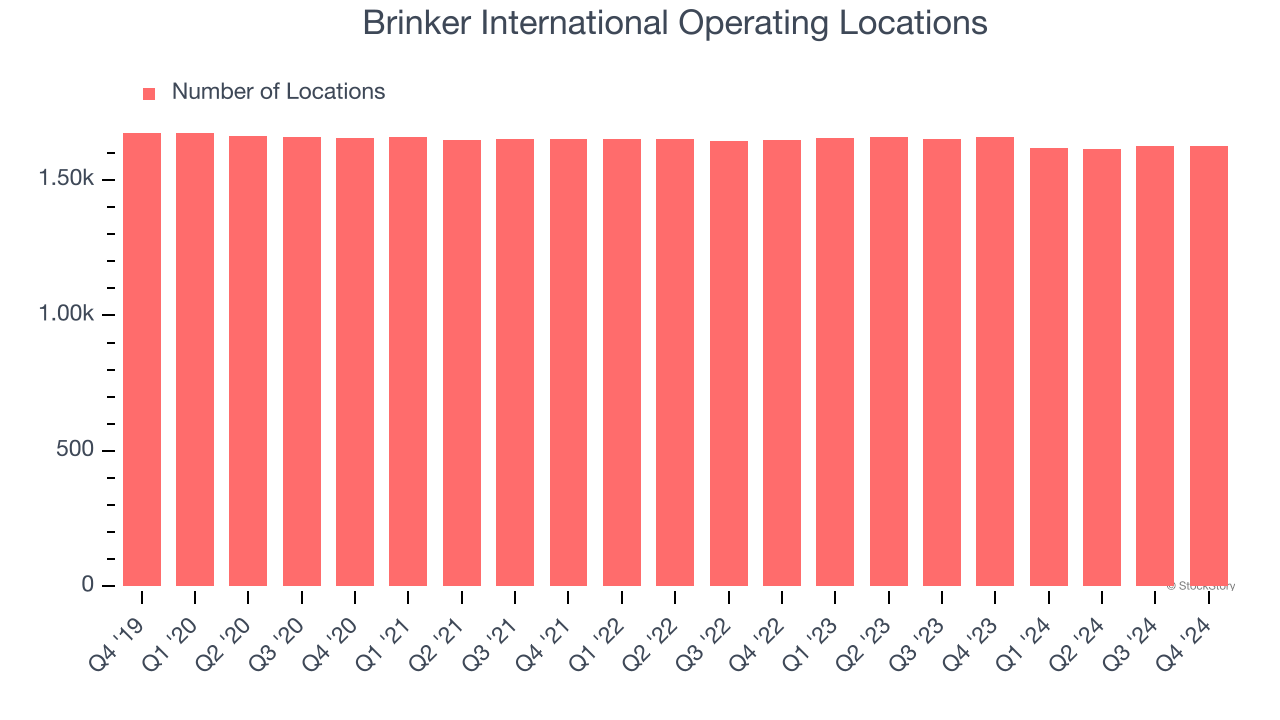

- Locations: 1,624 at quarter end, down from 1,658 in the same quarter last year

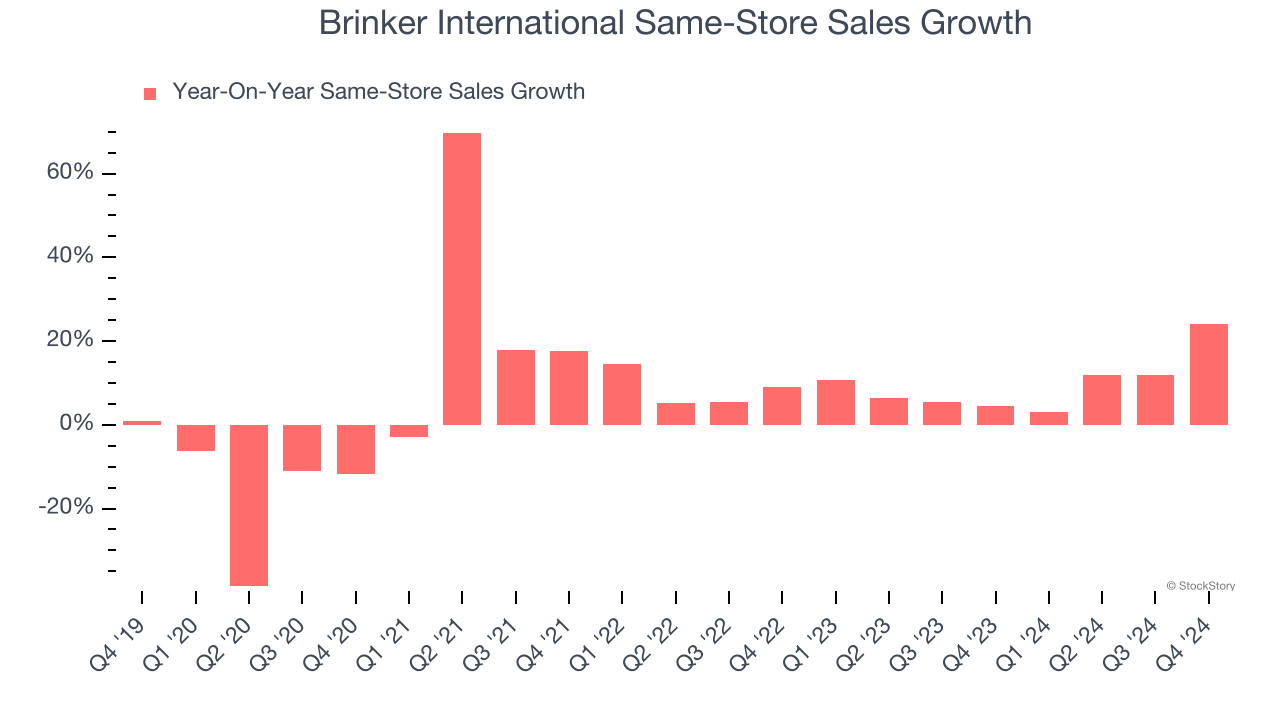

- Same-Store Sales rose 24.2% year on year (4.4% in the same quarter last year)

- Market Capitalization: $6.87 billion

"Improving fundamentals continues to drive a better guest experience and sustained business results," said President and CEO Kevin Hochman.

Company Overview

Founded by Norman Brinker in Dallas, Texas, Brinker International (NYSE:EAT) is a casual restaurant chain that operates under the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years.

Brinker International is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Brinker International’s sales grew at a decent 7.7% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) despite not opening many new restaurants, implying that growth was driven by higher sales at existing, established dining locations.

This quarter, Brinker International reported robust year-on-year revenue growth of 26.5%, and its $1.36 billion of revenue topped Wall Street estimates by 9.6%.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, a deceleration versus the last five years. This projection doesn't excite us and implies its menu offerings will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

Brinker International listed 1,624 locations in the latest quarter and has kept its restaurant count flat over the last two years while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Brinker International has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 9.8%. Given its flat restaurant base over the same period, this performance stems from a mixture of higher prices and increased foot traffic at existing locations.

In the latest quarter, Brinker International’s same-store sales rose 24.2% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Brinker International’s Q4 Results

It was good to see Otis narrowly top analysts’ revenue expectations this quarter on slightly better-than-expected organic revenue. On the other hand, its EBITDA missed. Adding to the bad news, its full-year revenue and EPS guidance both fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.9% to $93.05 immediately after reporting.

Indeed, Brinker International had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.