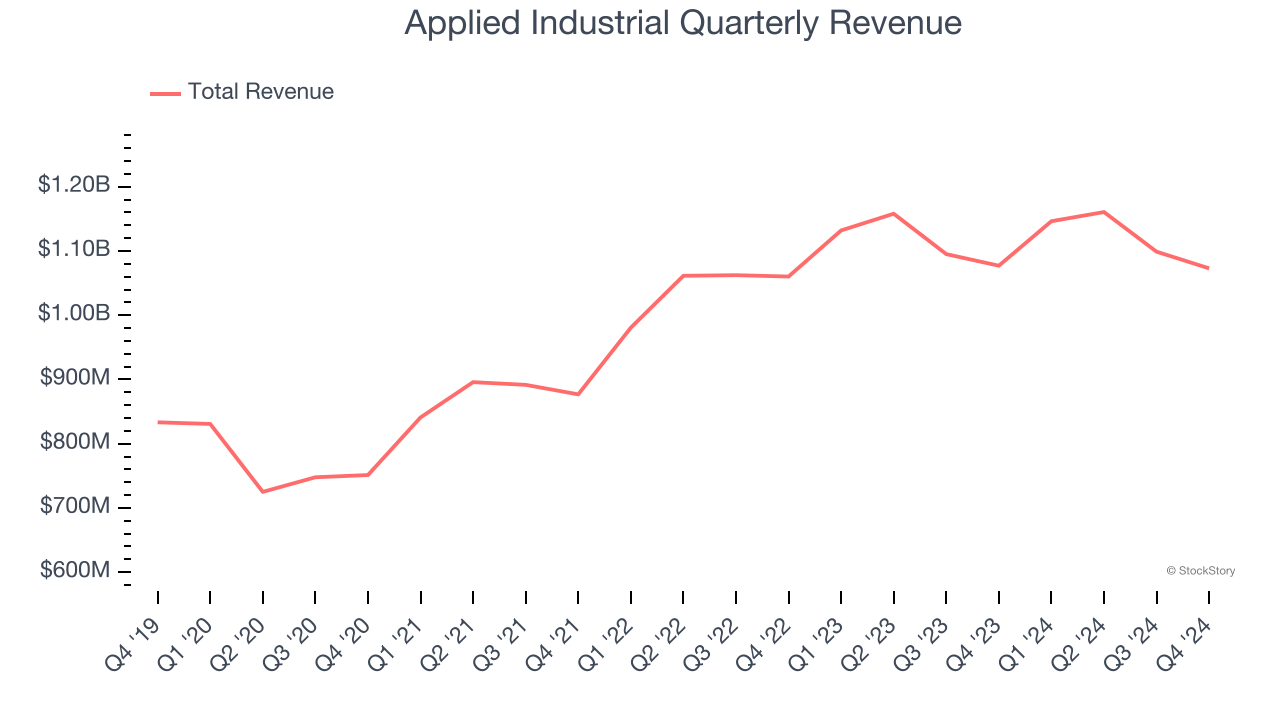

Industrial products distributor Applied Industrial (NYSE:AIT) met Wall Street’s revenue expectations in Q4 CY2024, but sales were flat year on year at $1.07 billion. Its GAAP profit of $2.39 per share was 8% above analysts’ consensus estimates.

Is now the time to buy Applied Industrial? Find out by accessing our full research report, it’s free.

Applied Industrial (AIT) Q4 CY2024 Highlights:

- Revenue: $1.07 billion vs analyst estimates of $1.08 billion (flat year on year, in line)

- EPS (GAAP): $2.39 vs analyst estimates of $2.21 (8% beat)

- Adjusted EBITDA: $135.1 million vs analyst estimates of $127.6 million (12.6% margin, 5.9% beat)

- EPS (GAAP) guidance for the full year is $9.85 at the midpoint, roughly in line with what analysts were expecting

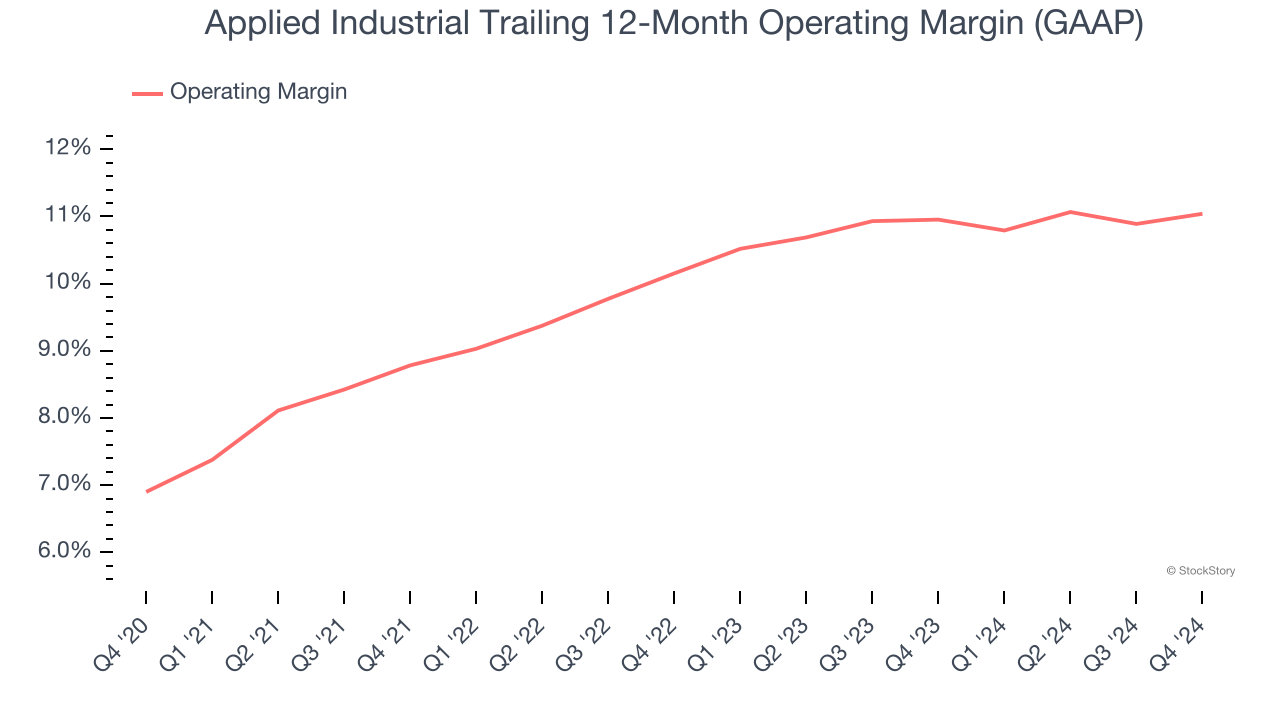

- Operating Margin: 11.3%, in line with the same quarter last year

- Free Cash Flow Margin: 8.9%, similar to the same quarter last year

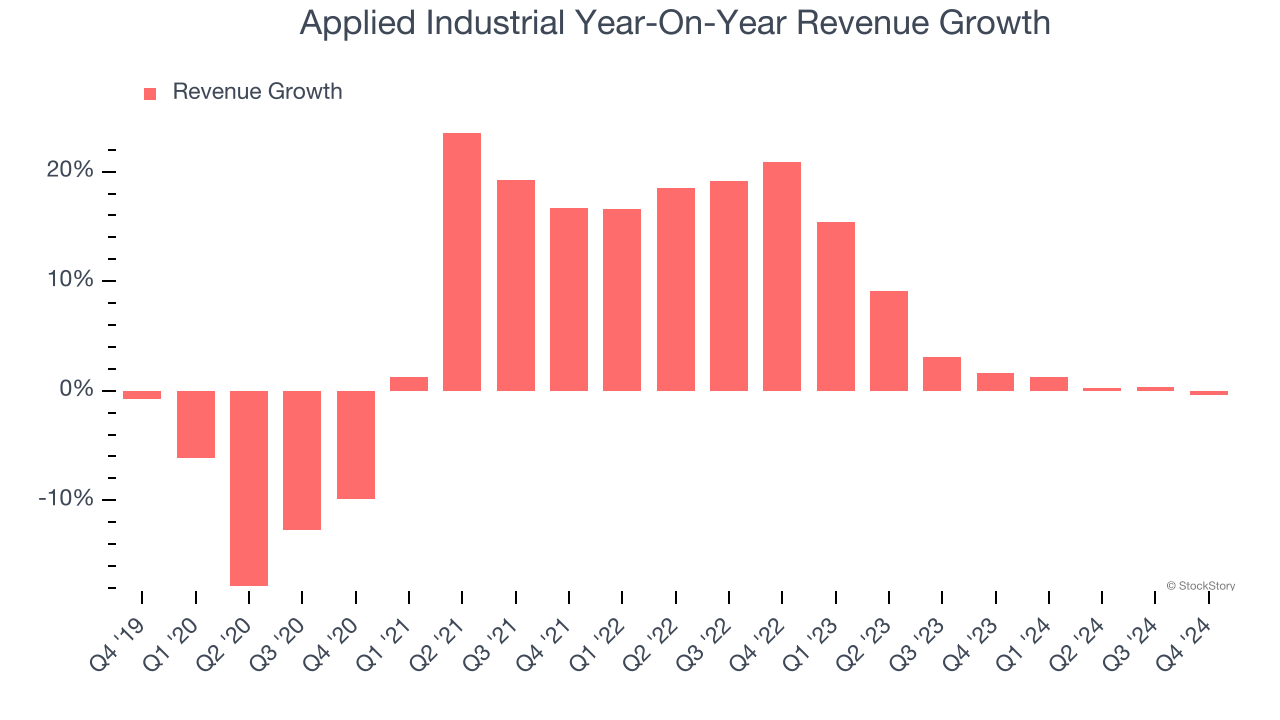

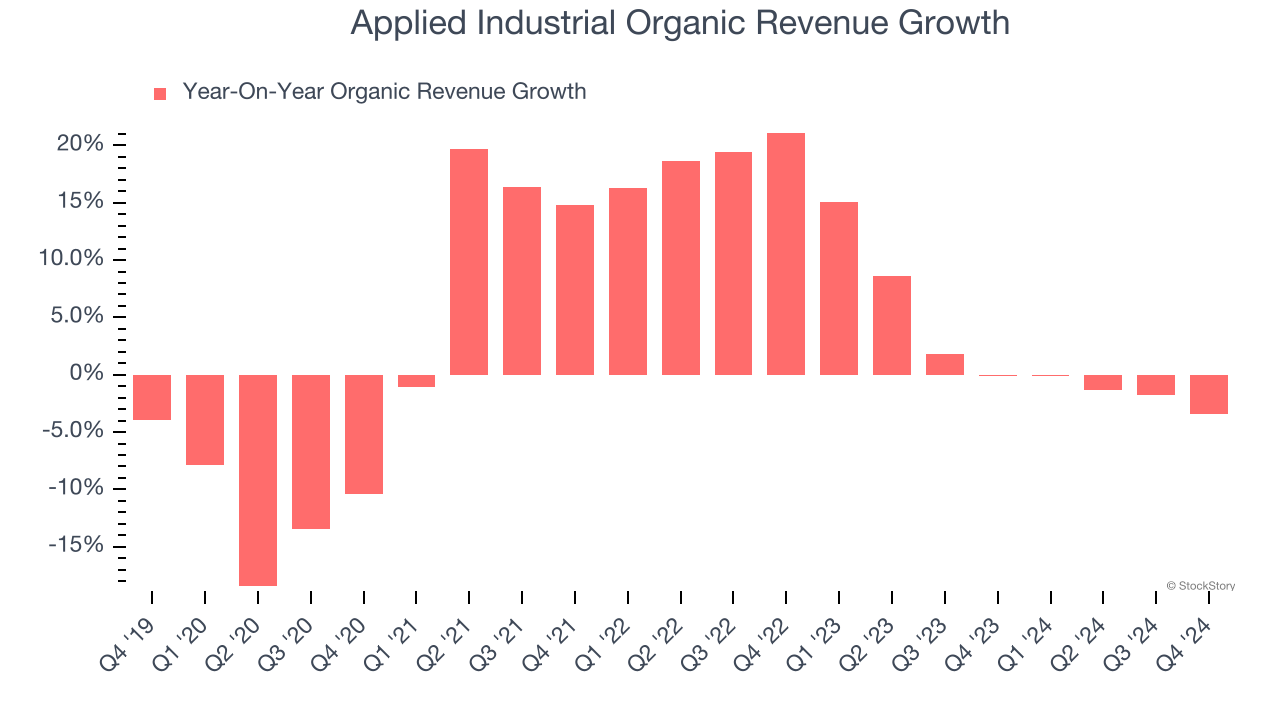

- Organic Revenue fell 3.4% year on year (-0.1% in the same quarter last year)

- Market Capitalization: $9.70 billion

Neil A. Schrimsher, Applied’s President & Chief Executive Officer, commented, “Fiscal second quarter EBITDA and EPS exceeded our expectations, increasing a respective 3% and 7% year over year on relatively unchanged sales. Demand remained mixed during the quarter with seasonal factors and holiday timing limiting customer activity in December. That said, our team continued to execute well with organic sales trends inline with our guidance, while strong gross margin performance and cost controls drove solid EBITDA margin expansion during the quarter. Additionally, the closing of our Hydradyne acquisition at the end of December represents another notable milestone in our story and provides solid growth and operational momentum moving forward. Overall, we had a productive second quarter that highlights our business resilience, self-help opportunities, and favorable industry position.”

Company Overview

Formerly called The Ohio Ball Bearing Company, Applied Industrial (NYSE:AIT) distributes industrial products–everything from power tools to industrial valves–and services to a wide variety of industries.

Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Regrettably, Applied Industrial’s sales grew at a tepid 5.3% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Applied Industrial’s recent history shows its demand slowed as its annualized revenue growth of 3.7% over the last two years is below its five-year trend.

Applied Industrial also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, Applied Industrial’s organic revenue averaged 2.3% year-on-year growth. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Applied Industrial’s $1.07 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, similar to its two-year rate. While this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Applied Industrial has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.8%, higher than the broader industrials sector.

Looking at the trend in its profitability, Applied Industrial’s operating margin rose by 4.1 percentage points over the last five years, showing its efficiency has improved.

In Q4, Applied Industrial generated an operating profit margin of 11.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

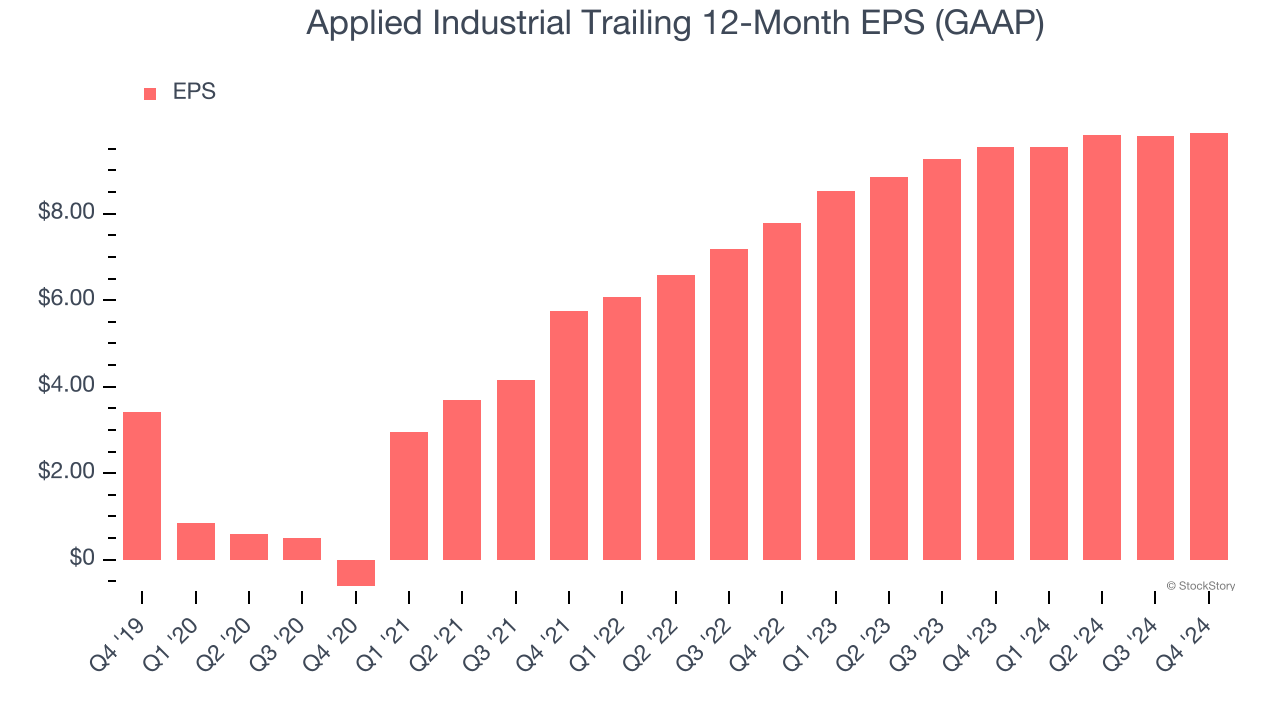

Applied Industrial’s EPS grew at an astounding 23.7% compounded annual growth rate over the last five years, higher than its 5.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Applied Industrial’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Applied Industrial’s operating margin was flat this quarter but expanded by 4.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Applied Industrial, its two-year annual EPS growth of 12.6% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Applied Industrial reported EPS at $2.39, up from $2.32 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects Applied Industrial’s full-year EPS of $9.87 to grow 2.6%.

Key Takeaways from Applied Industrial’s Q4 Results

We enjoyed seeing Applied Industrial exceed analysts’ EBITDA and EPS expectations this quarter. On the other hand, its organic revenue slightly missed and its revenue was in line with Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $250.22 immediately after reporting.

So should you invest in Applied Industrial right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.