Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Waste Management (NYSE:WM) and the best and worst performers in the waste management industry.

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

The 8 waste management stocks we track reported a softer Q3. As a group, revenues missed analysts’ consensus estimates by 2.1%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.1% since the latest earnings results.

Best Q3: Waste Management (NYSE:WM)

Headquartered in Houston, Waste Management (NYSE:WM) is a provider of comprehensive waste management services in North America.

Waste Management reported revenues of $5.61 billion, up 7.9% year on year. This print exceeded analysts’ expectations by 1.7%. Overall, it was a strong quarter for the company with a decent beat of analysts’ adjusted operating income estimates.

“The Company’s third quarter results again demonstrated the dedication of our people, the consistency of our business model, and the strength of our operations,” said Jim Fish, WM’s President and Chief Executive Officer.

Waste Management pulled off the biggest analyst estimates beat of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $208.80.

Is now the time to buy Waste Management? Access our full analysis of the earnings results here, it’s free.

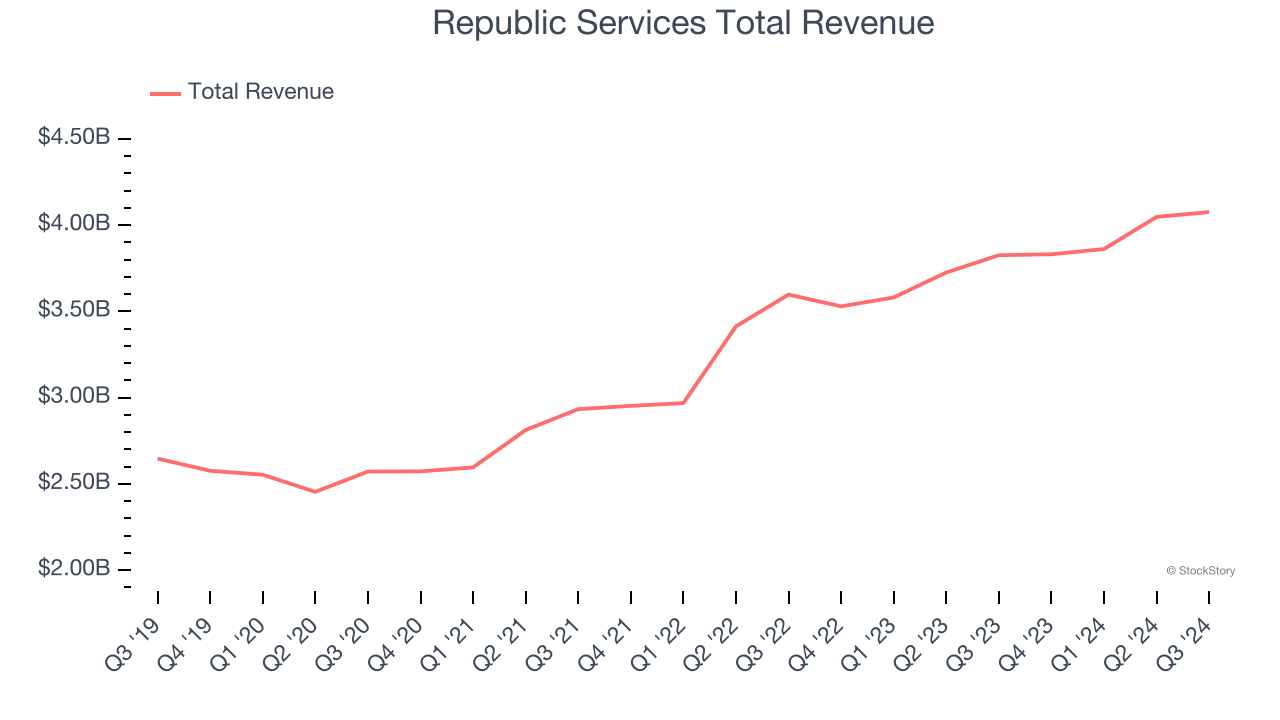

Republic Services (NYSE:RSG)

Processing several million tons of recyclables annually, Republic (NYSE:RSG) provides waste management services for residences, companies, and municipalities.

Republic Services reported revenues of $4.08 billion, up 6.5% year on year, falling short of analysts’ expectations by 1%. The business performed better than its peers, but it was unfortunately a mixed quarter with an impressive beat of analysts’ adjusted operating income estimates but a slight miss of analysts’ sales volume estimates.

The market seems content with the results as the stock is up 3.7% since reporting. It currently trades at $211.83.

Is now the time to buy Republic Services? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Quest Resource (NASDAQ:QRHC)

Recycling corporate waste to help companies be more sustainable, Quest Resource (NASDAQ:QRHC) is a provider of waste and recycling services.

Quest Resource reported revenues of $72.77 million, up 3.3% year on year, falling short of analysts’ expectations by 5.6%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

As expected, the stock is down 29.8% since the results and currently trades at $5.78.

Read our full analysis of Quest Resource’s results here.

Enviri (NYSE:NVRI)

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE:NVRI) offers steel and waste handling services.

Enviri reported revenues of $573.6 million, up 9.3% year on year. This number lagged analysts' expectations by 6.5%. Overall, it was a disappointing quarter as it also produced full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

Enviri had the weakest performance against analyst estimates among its peers. The stock is down 6.7% since reporting and currently trades at $9.37.

Read our full, actionable report on Enviri here, it’s free.

Casella Waste Systems (NASDAQ:CWST)

Starting with the founder picking up garbage with a pickup truck he purchased using savings from high school, Casella (NASDAQ:CWST) offers waste management services for businesses, residents, and the government.

Casella Waste Systems reported revenues of $411.6 million, up 16.7% year on year. This result met analysts’ expectations. Taking a step back, it was a softer quarter as it produced a significant miss of analysts’ adjusted operating income estimates.

Casella Waste Systems pulled off the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is up 3.1% since reporting and currently trades at $104.40.

Read our full, actionable report on Casella Waste Systems here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.